I built this chart by combining VOD (video on demand) data available in Ofcom‘s Media Nations and filling in the blanks from the underlying data.

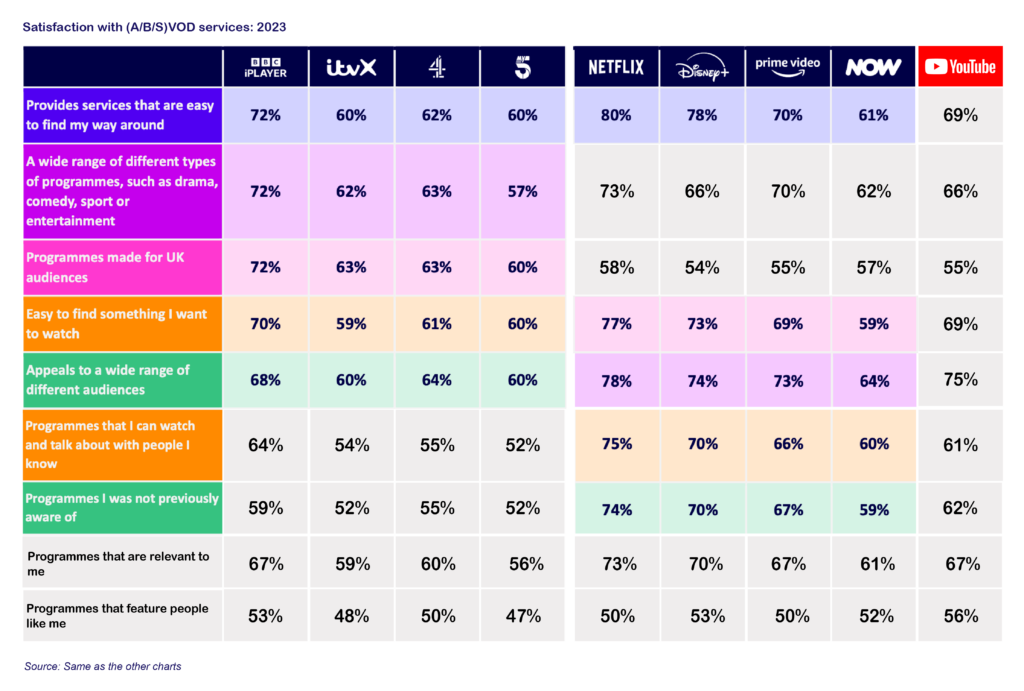

It’s an interesting comparison, despite the B or S (BS??) variance in VOD type. Though it’s odd to me to have excluded YouTube which also sat in the same dataset.

A couple of thoughts..

This multiple app route is going to start creating issues as users get tired of switching apps and using various machinations of recommendations and search funcitons to find something to watch,

I’ve now settled on two or three services which i’ll browse for and generally find something that i’m happy to watch,

Without a common discovery UI (like the EPG) this will start creating challenges for new entrants to make a successful entry and then grow,

Freely is clearly a potential answer here depending on how and how far it rolls out. It does make me think of what a short-sighted decision it was to kill Kangaroo all that time ago!

You can see why YouTube is posing such a threat to TV attention with high satisfaction scores across product and content metrics. Whether it’s ‘broadcast quality’ content or not, audiences are clearly satisfied with it and score it particularly highly for programmes that are relevant to me and featuring people like me.

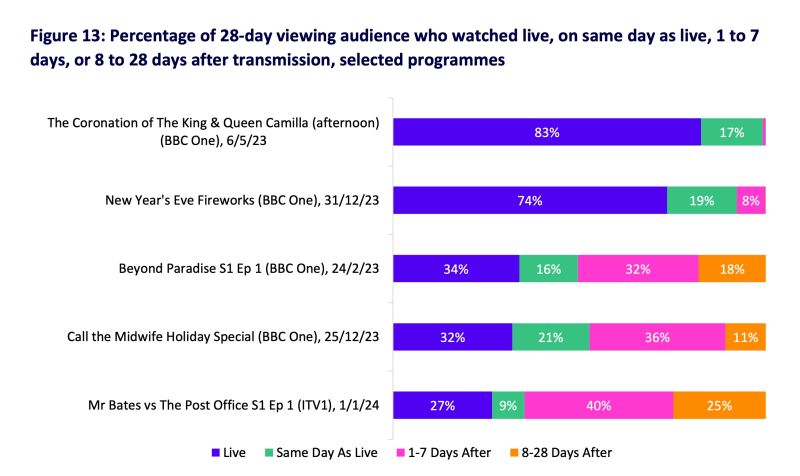

But for me, one outstanding stat was that 8% of the 12.1m people (yes that’s nearly a million people!) watching the New Year’s fireworks are doing so 1-7 days after New Years Eve! Call me a party pooper 🎉 but I struggle to watch fireworks live in person, let alone on telly and absolutely not as catch up! #mindblown 🎇

ITV results were announced yesterday with what I thought was a solid half-year performance. The core mission, transforming their linear business into digital, is going well and they’re well on their way to £750m digital in 2026, although growth did slow a touch in this period.

…Non-digital advertising was even up slightly (£48m / 7.6%) in H1 24. However, with the Euros and standout hits like Mr. Bates, I’m not convinced a true like-for-like comparison would be as flattering.

Their other goal, expanding studios, took a hit for various reasons. These issues will resolve over time, but the underlying concerning statistic for me was the percentage of revenue coming from streamers, which fell to 22% (from 29%). While internal delivery remains a significant income, if they’re not converting new streamer business, relying on other FTA broadcasters in similarly difficult markets (who are potentially less well run), will make substantial growth tricky.

While their digital conversion is progressing well, and it’s clear the business is well-managed, it strikes me their ultimate goal doesn’t seem particularly exciting. Surely being anything other than the ‘#1 Commercial Broadcaster Video On Demand Platform’ would be a failure for the clear #1 Commercial Broadcaster. At best, replacing linear revenue with digital revenue will give or take result in a business of the same size.

Other options? 1. 𝗠𝗮𝗿𝗸𝗲𝘁 𝗖𝗮𝗽 𝗢𝗽𝗽𝗼𝗿𝘁𝘂𝗻𝗶𝘁𝘆: ITV’s Market Cap (£3.1B) is still a bargain for a well-run broadcaster reaching 40m-45m each month and a successful digital platform with 14.6m MAUs and 1m subs. The worst move would be to rebrand it. ITV is a longstanding, loved brand in tune with it’s audience. But a significant and serious catalogue could fall in behind them to make an immediate, serious international move. Sadly, that’s not usually how these things go. 2. 𝗔𝗰𝗾𝘂𝗶𝘀𝗶𝘁𝗶𝘃𝗲 𝗚𝗿𝗼𝘄𝘁𝗵: Being in a strong financial position, not overly leveraged, they could become acquisitive themselves. Anything stateside might be challenging but there are plenty of interesting EMEA targets. Applying their demonstrably effective management approach to other media groups could yield value, particularly if combined with… 3. 𝗔𝗴𝗴𝗿𝗲𝘀𝘀𝗶𝘃𝗲 𝗗𝗶𝗴𝗶𝘁𝗮𝗹 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝘆: ITV emphasised the importance of their FTA digital play (vs. Subscriptions). How about stop playing nice with your peers (Freely), acquire a larger catalogue(s) and build out a major European commercial VOD platform? Their massive FTA audience could be upsold into a deeper experience and could be an opportunity if scaled across multiple substantial markets.

All that said, kudos to ITV. These are solid results, and while I wonder if they could be more aggressive, you can’t underplay the skill with which they’ve executed their plan. Any one of my options would add significant distraction.

Last week when looking at ITV’s annual report I suggested that News could be an opportunity for them based on what I perceived to be a relatively insular (ITVX focussed) strategy..

It got me thinking about how much of a greenfield opportunity Digital News is on new digital and social platforms. So I’ve spent the last week or so looking at the various iterations of legacy news operations and how they’ve been applied on these platforms. This all in advance of Ofcom‘s new News Consumption Survey which is due next month (May).

Some headlines…

As it stands, The Daily Mail has the most effective overall social digital media strategy, although it feels quite disjointed and leads to a confusing brand picture.

I find BBC News’s performance particularly lacklustre given their position as the UK’s number 1 media brand and the global influence they aspire to exert.

The philosophical approach by our PSBs and some legacy media risks ceding control of the social news agenda to new entrants (GB News) whilst it’s importance continues to grow.

There’s a significant upside opportunity for mainstream news brands to engage an already huge and growing audience.

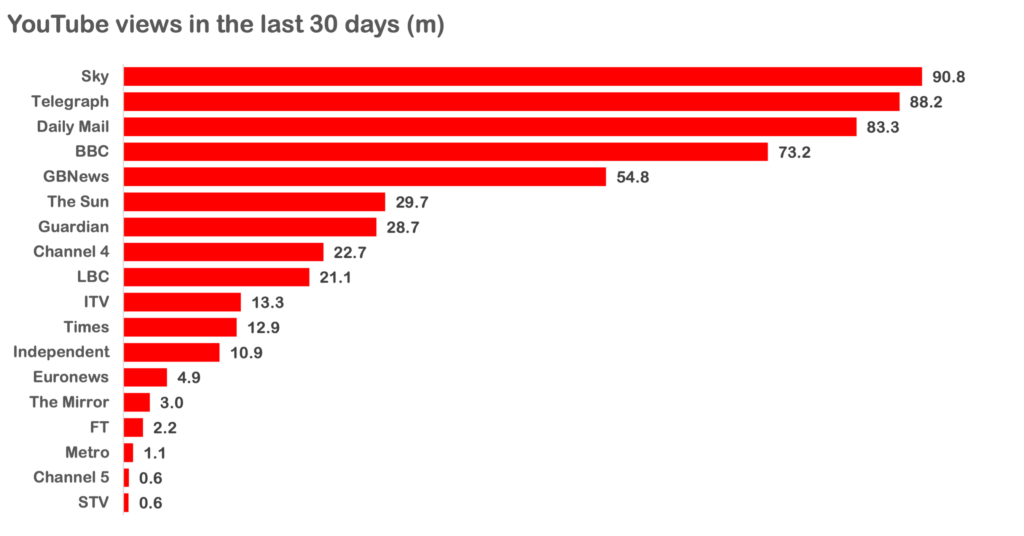

YouTube

YouTube views, last 30 days, courtesy of Social Blade

On YouTube, brands tended to follow one of two paths. Of the top performers, Sky News, BBC News and GB News employ an approach faithful to their overall editorial. Whereas the Telegraph’s and Daily Mail’s YouTube channels seem to bear little resemblance to any cohesive editorial strategy. That’s not to say they’re not engaging, but I struggle to see how generic syndicated news clips deliver any real value to their brand.

Sky was most impactful, delivering a high volume of content, including live-streams of their linear output, although I still feel there’s a HUGE opportunity in creating bespoke platform specific content tailored for this audience rather than simply clipping traditional linear output. We always found there was huge upside in leveraging the intelligence from usage data to optimise content with the specific platforms and audiences in mind. The BBC has some nice bespoke content on their ‘Shorts’ page but generally just post clipped content from their linear feed.

Overall, I found GB News’ approach to be the most adapted to the platform with a specific thumbnail strategy, some bespoke content, super high volume and use of live and a extremely faithful editorial output (if somewhat predictable and click-baity).

I guess YouTube uses red too?

The Sun has built some bespoke content although rather than lean into audience and platform specific trends, they’ve taken a very traditional / formal ‘suits behind a desk’ approach presenting an audio visual case study of why you shouldn’t allow marketing or brand people to design sets.

Overall I find the YouTube numbers underwhelming. Despite the BBC being one of the best known English language news services in the world and allegedly being the most visited English language website, it’s only 197th in Social Blades list of YouTube’s impactful news channels (only 6 of the legacy UK services I reviewed appear at all in the top 500!). With the amount of content and resources at their disposal the BBC should be aiming north of 500m monthly views and could probably get closer to 1Bn.

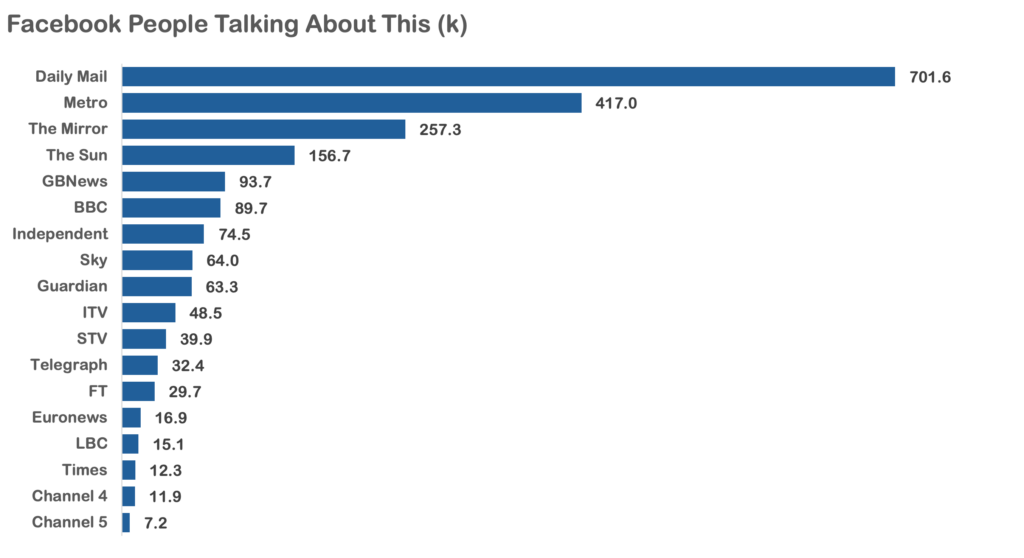

Facebook

Facebook, People Talking About This, courtesy of Social Blade

On Facebook I used their ‘People Talking About This’ stat as a comparative measure of currency and impact. Almost exclusively, News brands are using Facebook as a discussion board and link farm to drive people back to their owned websites and apps.

The Daily Mail are stand out leaders with a strategy of ridiculously high post volume (close to 10 every hour). Unlike their YouTube, it’s really faithful to their core digital editorial output and given the tabloid nature of the content, seems to generate a fair amount of discussion amongst the Facebook-crowd. Perhaps unsurprisingly, other tabloid titles dominate the top performers with all employing a slightly less effective version of the Mail’s strategy.

Instagram

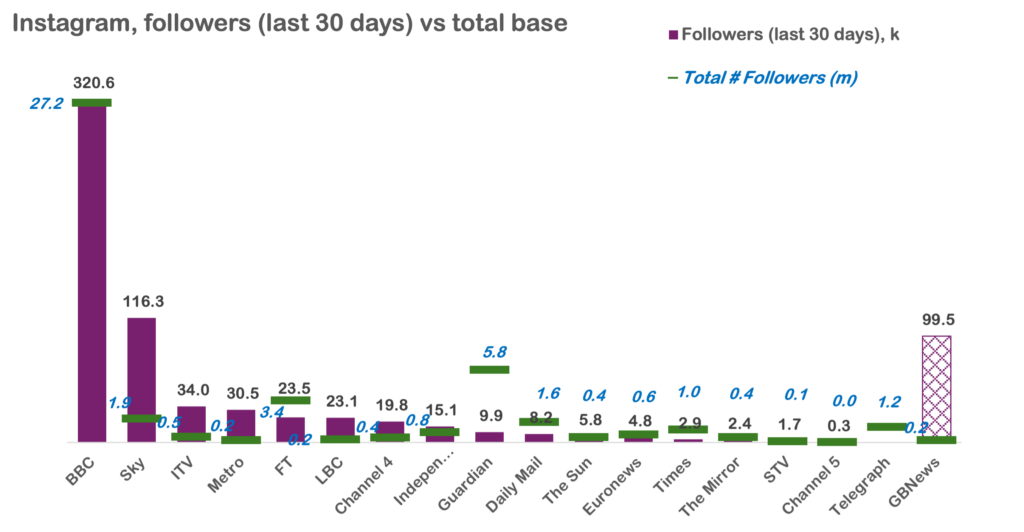

Insta followers, last 30 days and total, courtesy of Social Blade

I personally struggle to recognise Instagram’s suitability as a viable news platform, but it’s mass media scale dictates audiences will consume it there regardless. The stats are difficult to interpret and the strategies quite unique. My analysis was centered around the main pages for legacy brands although brands (e.g. BBC News) often employ tens of different Insta accounts, a varying mix of images and reels, some video focused, whilst others clearly using picture editors to focus on image quality. I’ve considered multiple benchmarks.

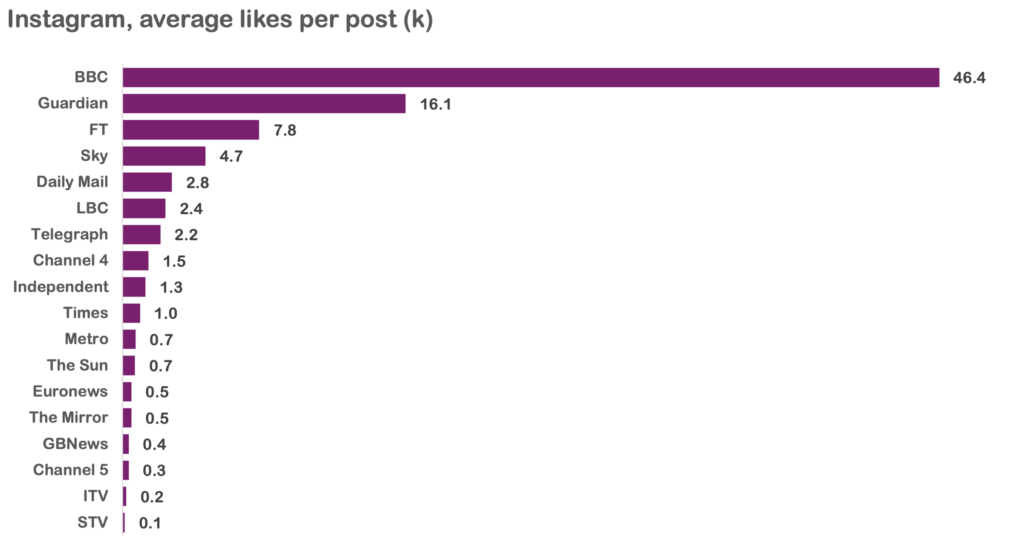

Instagram average likes per post, courtesy of Social Blade

BBC News is the stand out leader with a massive 27m followers, 320k incremental followers within the last 30 days and 46.4k avg. likes per post. The Guardian and FT have impactful strategies leaning into the aesthetical nature of the platform. They have large follower numbers (5.8m & 3.4m) and are gaining large amounts of likes per post (16.1k and 7.8k) but they’re not posting very much (maybe once a day) and so any follower movement in the last 30 days is muted. Sky have a mixed picture editor / video strategy, are quite active in posting and generating significant engagement (likes per post) evident not only large in total follower numbers (1.9m) but also in terms of last 30 day movement (116k). GB News’ data is broken (via Social Blade) for the last 30 days and massively overstates their recent impact, they have 193k followers who aren’t particularly engaged (400 likes per post). Whilst extremely active, they’re basically using it as a video distribution platform.

I quite like what ITV and the Metro are doing. ITV has bespoke content (via Reels), although I’d like to see them fully adapt and replace the clipped linear content on the main feed. Metro have also developed quite a nice style leaning into platform functionality to mix the use of images, text and video quite effectively. Both strategies seem to be working with decent follower movement in the last 30 days.

TikTok

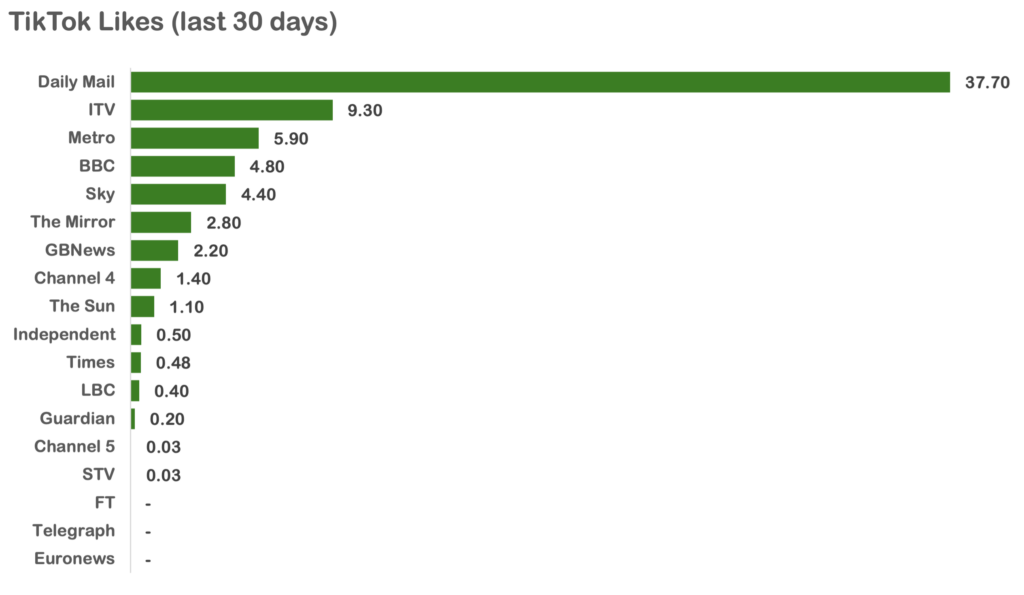

TikTok, likes in the last 30 days, courtesy of Social Blade

The Daily Mail has the largest and most engaged base on TikTok, but again has a unique editorial for this individual platform (this time a US-centric celebrity gossip focus). I’m sure there must be logic in their overarching strategy (they won’t cannibalise each other?) but it doesn’t feel additive to a consistent brand message from where I’m sat. You can’t deny they’ve achieved success and scale, although I note their digital revenues seemed to have flatlined last year and it will be interesting to see how they react to this. ITV are posting some of the bespoke content seen on their Insta, but again I’d like to see them take a wholly bespoke approach, engaging the audiences they’ve started to build. Metro are also making bespoke content but have a much lighter posting schedule, delivering the same impact (in likes) with only 10% – 20% (2/3 post per day) of the content output of the Mail, ITV, Sky or the BBC. BBC and Sky are still largely just clipping linear content albeit with some light post-production customisation and would do well to experiment with more bespoke content.

Owned platforms vs Social Media

Many of the PSBs and legacy news brands opt to favour their own platforms as a focus for their digital efforts based on an ability to own the data and/or monetise them more effectively (and not share any of that revenue). Whilst I can understand that, I don’t believe the PSBs do news entirely for commercial reasons and certainly I find the BBC’s philosophical approach here slightly odd given they don’t have the same commercial restrictions. All that said, I don’t believe social content particularly cannibalises other consumption and so would recommend a more active and innovative strategy to engage this growing audience. In fact, when you have a cohort of the population growing up away from traditional media channels, active social content strategies could be an important route to seed and build relationships between consumers and legacy brands that blossom into deeper direct consumption relationships further down the road.

Methodology

I looked at various legacy broadcast and publishing news services across YouTube, Facebook, Instagram and TikTok using Social Blade for my analysis trying to get reasonable metrics to assess currency and engagement. I pulled the data on the 3rd and 4th of April and so depending on lag of data feeds by platform the 30 day periods reviewed were consistent for comparative purposes and generally had most of March and possibly a few days of February. I reviewed The Independent, The Guardian, The Telegraph, Financial Times, Daily Mail, The Times, The Sun, BBC News, Channel 4 News, Channel 5 News, ITV News, Sky News, STV Group plc News, Euronews , Daily Mirror, Metro.co.uk, Global‘s LBC and GB News. To be clear, I’ve just been looking at the presentation of these services, not passing judgement on the status or quality of their journalism, nor have I tried to take a position on the bias of their output. I now need to go and purge my browsing history so I can get back to being fed golf clips rather than the various iterations of news the algorithms now think I’m interested in!

ITV Results came out via it’s annual report last week. I always find these interesting, often more for the information that’s not included, rather than the info that is!

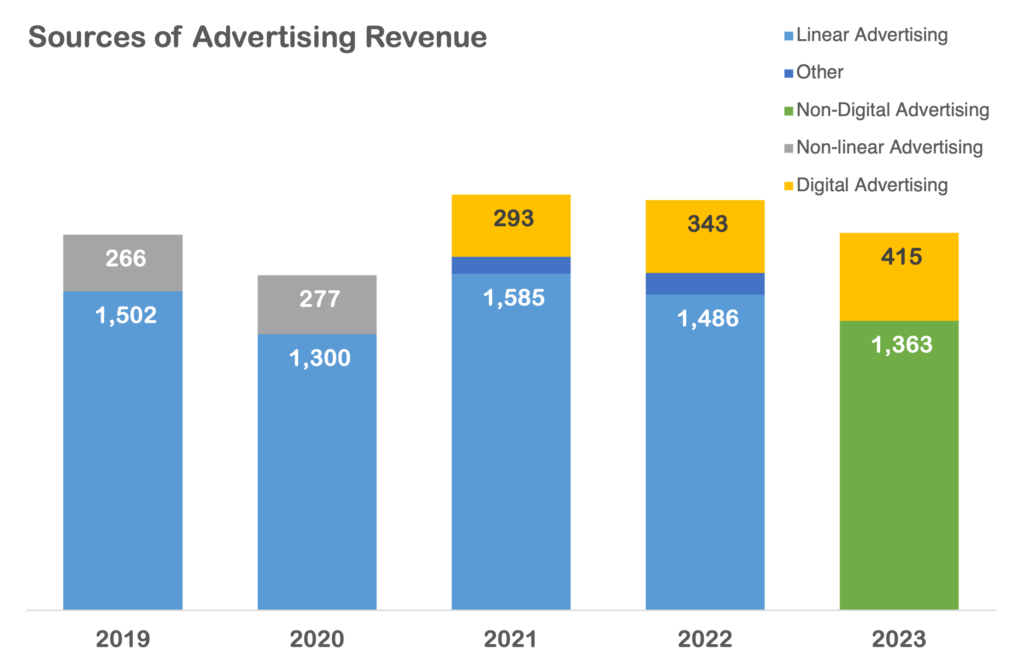

Last year ITV very helpfully included data on linear advertising revenues (‘Linear Remains Resilient’). With declining resiliency, they’ve opted not to do that this year but we can still piece together the picture. Linear will have delivered nearly £1,363m in 2024, not far above 2020’s Covid ridden performance. Q1.24 is apparently better, 3% up YoY (although 23 is a shitty baseline). We won’t see their detailed quarterly phasing for a couple of months, but if they’re hitting their projected 15% increase in digital income, this would probably still see a marginal YoY decline in linear.

2024’s green bar of ‘Non-digital Advertising’ may include a 0% – 5% overcount in Other advertising which was apparent when they reported both linear and digital advertising in 21 & 22.

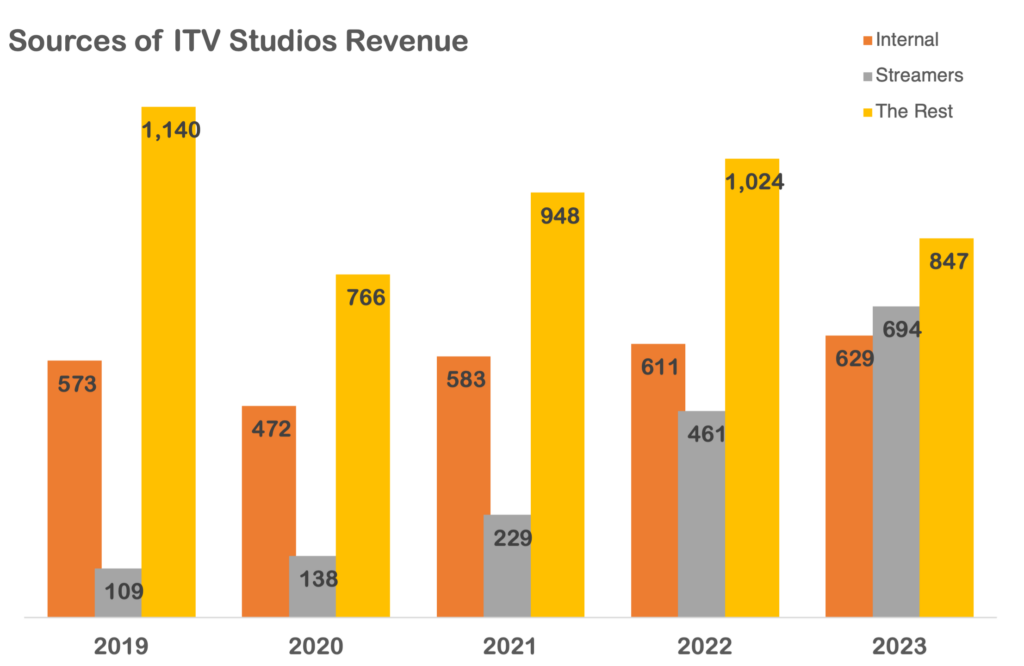

ITV Studios is without doubt a success story for ITV, growing substantially over recent years. They called out growth they needed with global streamers, and they’re hitting their target. They also produce a lot for their own internal channels but it was everything else they produce which I found interesting. 2023 saw a 17% decrease YoY in revenue from other (non-internal, non-streamer) broadcasters. From the chart it’s not a clear trend, at best you could call it ‘volatile’. But revenue diversity is important and it will be interesting to see how this develops.

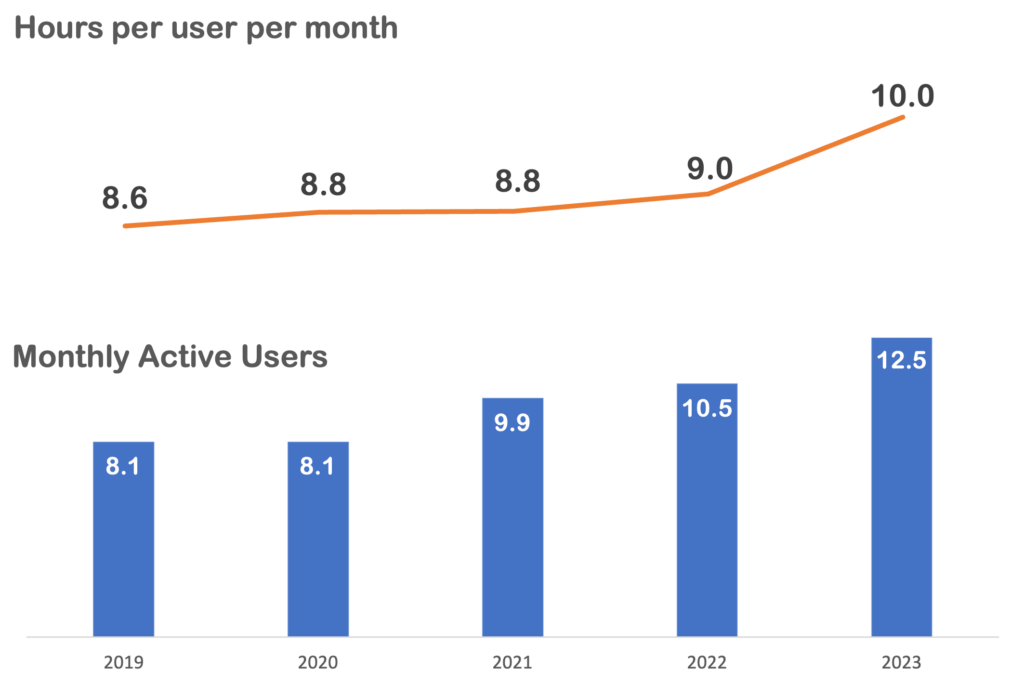

ITVX growth has also been impressive. Growing to 12.5m monthly active users with each user watching incrementally more! Sadly I don’t have full access to BARB anymore but you can pull together a reasonable proxy for linear from publicly available data. By my reckoning, ITV’s linear Monthly Active Users (or reach) in 2023 was 45m and they streamed a total of nearly 8Bn hours, or the equivalent of 14 hours per user per month. Compared against the 12.5m MAUs streaming 10 hours a month on their digital service.

ITVX User base and consumption

I have 2 perspectives on this..

If you consider how much revenue is generated for each platform, that makes a digital hour (£0.33) nearly twice as valuable as a linear hour (£0.17). This is impressive and makes sense, with a more engaged and younger audience switching to digital first, coupled with an enhanced ad product. You would expect this differential to reduce as reach expands but I don’t think you’ll lose it all! There is also a potential Newtonian impact to consider, with linear audiences devaluing as higher value (engaged / younger) audiences migrate online

Secondly, ever since i can remember, ITV has been a massive and ubiquitous media presence; 45m (70%+) monthly reach . As the move to digital accelerates what will be the impact on the brand and particularly their ad business as they transition to become one of many niche (is that too harsh?) suppliers of admittedly excellent long-form content. How large can a walled garden owned platform grow on a £1.3Bn content spend?

So what would I do?

Honestly, i think ITV are doing a really good job but this is where i’d look to enhance their plan…

I’m not sure there’s anything you can do about linear, there’s only so much you can do within a market that’s turned. If they can continue to replace linear with more effective digital revenues then shareholders should be happy.

The growth in Studios has been really impressive, but if you dig in to an average consumers viewing day (4hrs 28 of video mins consumed daily), ITV Studios is only addressing 74% of the market (52% looking at 1634s). Video sharing platforms are becoming increasingly dominant and any major supplier of content should be figuring out how to supply content into that space too. There should be (maybe there already is tbh) a target on non-longform, potentially non-video content production. Whilst naturally easier to monetise audiences effectively on ITVX I would set targets and budgets to create bespoke scripted and non-scripted content for social platforms to learn how to deliver compelling stories in new ways, how to monetise them effectively, and also to up-skill Studios and create a calling card for more non-traditional 3rd party service work.

It’s great they called out the News experience on mobile, this feels like a real opportunity! There’s some bespoke presentation on TikTok, but it leans towards to the more pop-culture end of the news. ‘Proper’ news still seems to be mostly grey suits behind a desk, clipped from the linear programme. It’s time to lean into their established quality journalism, and really play with presentation of news across new platforms to adapt it for new and younger audiences (I don’t mean just having a presenter with scruffy jeans!).

Content is always king, but i’m afraid an Oscars live event and Celebrity Big Brother don’t cut it as tent pole events to ‘supercharge streaming’. M&E EBITDA margins may be challenged (<10% in 2023) but they need to capitalise on the momentum they have with ITVX. Interestingly both Netflix and Amazon having been diving into sport as a important genre for streamers and it scratches an itch for many that can’t easily be replaced with other forms of content. ITV have a strong sporting heritage and I would be looking to potentially invest in this as a route to drive more viewers into ITVX.

I’m still buzzing after our second live show last night. Our resident 4Music DJ, Shortee Blitz, smashed another set out of the park crunching together some bad ass tunes whilst whipping up a social media storm that, at one point, had us trending #1 worldwide on twitter.

The idea started as just trying to inject some pace on our channels and mix together some of our playlist videos, when Shortee sent us a mix that he’d done using the new Video DJ software from Serato. I loved it, the thought that we could have someone with Shortee’s skills live mixing videos like that was awesome. Naturally we thought… ‘well let’s do it live live then!’ We only finished building our studio less than six months ago and had never really conceived of it with the idea of doing live TV broadcasts from the office, but with a little bit of head scratching and arm twisting we worked out that it was possible and wasn’t going to cost the earth.

I honestly believe that no-one has EVER done music TV like this – it’s so fresh and raw with so much energy. Shortee is amazing, the way he mixes, scratches and beat juggles his way thorough the videos is spellbinding. The response we’ve had back via social media has been unreal – last night we did nearly 6k tweets with just an amazing feeling of positivity and love from everyone getting involved (including a lot of well deserved love for Shortee).

Where do we go from here? We have another couple of shows this year (Friday’s at 8:30 on 4Music) and are defenitely keen on bringing it back next year. There maybe some tweaks to the format and we’d love to get a few more DJs involved. We’re also thinking about getting a few exclusive performances recorded that Shortee can mix into the set, but I’d love to get a live audience involved too – i know my team won’t thank me for trying to do live TV in a club but it seems like a natural evolution from where i’m sat.

So do tune in and see what it’s all about. We love making the show and the energy really blasts out the other side of the screen.

Just a final big shout out to Shortee and all of my team who have worked like mad to get the thing on-air.